Arkil

Introduction

Arkil Holding A/S is a Danish-based engineering and construction company with headquarters in Haderslev. The company is engaged in various types of construction works, performs asphalt surfacing and maintenance, foundation and marine construction and road service. Besides Denmark, Arkil also operates in Germany, Ireland and Sweden. The company has 1.166 employees and the revenue for 2013 was 2.776,4

million DKK. The foreign part accounted for a total of 29 % of revenues. Arkil’s expectations for 2014 are revenue of 3.000 million DKK. and a profit before taxes between 50-80 million DKK.

Valuation

Our DCF analysis is based on the free cash flow approach which assumes that shareholder wealth is directly related to the free cash flows generated by the company. In order to compute the free cash flow of Arkil the main drivers in the model has been forecasted: net profits, depreciations, CAPEX and net changes in net working capital.

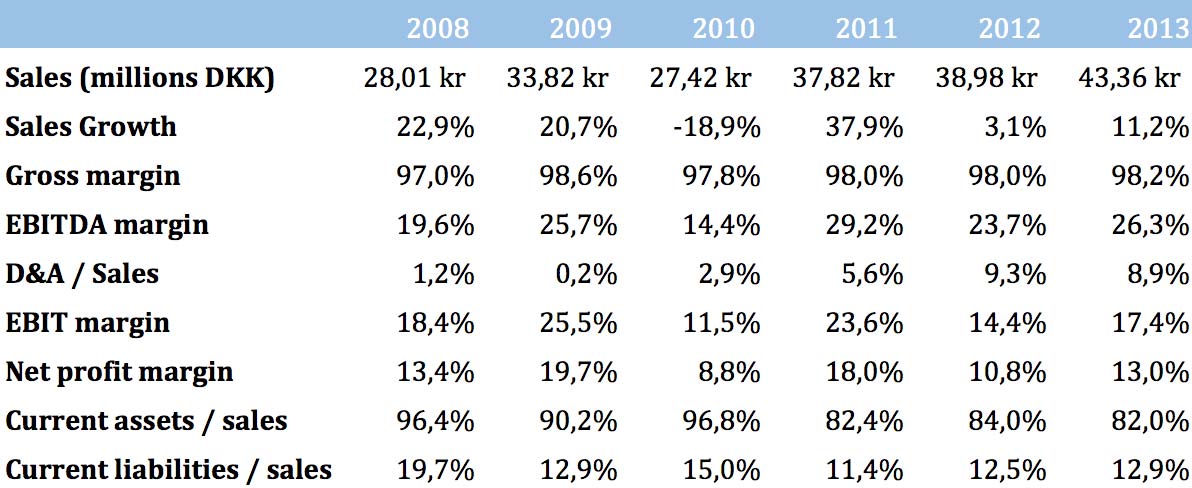

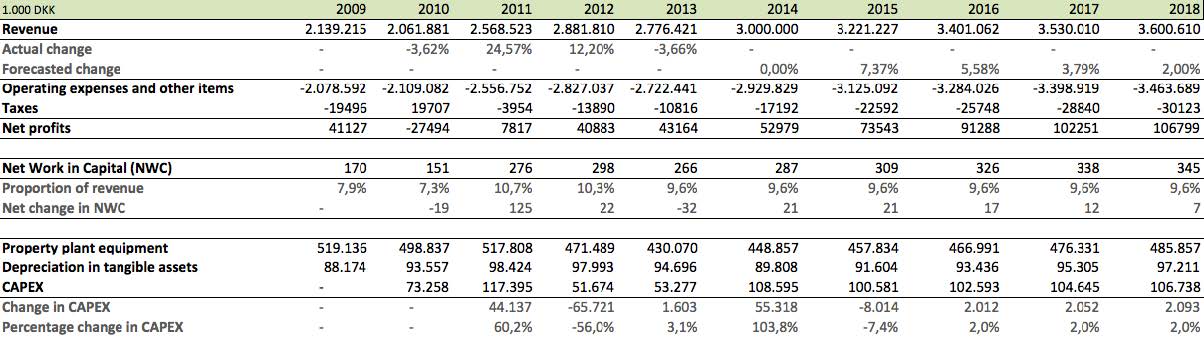

In the revenues forecast we start out with revenues for 2014 of 3.000 million DKK equal to Arkil’s own expectations for the year. A future revenue growth of 7,4% in 2015 is assumed based on the 2010-2013

mean. This growth rate is from 2015-2018 set to fade linearly to 2% – our long-run growth rate. The associated costs are forecasted in a similar manner, however company marginal taxes rates are set to 23,5%

in 2015 and 22% hereafter in accordance with proclaimed tax rules. This provides a net profit forecast asseen in the table below.

To forecast the net changes in net working capital of Arkil we notice from the table below that net working capital the last 3 years approximately has been a fixed percentage of revenues. We therefore set future net working capital equal to this fixed percentage and thereby get forecasted net change in net working capital.

The depreciations are assumed to remain on the 2013 level since there have only been small variations in the item and no obvious trend in the past years. Further, CAPEX is set to fade to this level in order to ensure

balance between the two items in the terminal part.

To sum up, the forecast for the main drivers is seen below.

We use a WACC of 9%, which again is reasonably conservative.

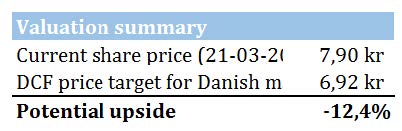

Computing the free cash flows and doing the valuation we get share price of DKK 1.727,58, which compared to the actual share price of 26-05-2014 of DKK 865 equals an up side of 99,7%.

![]()

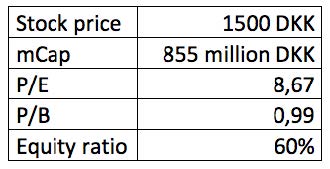

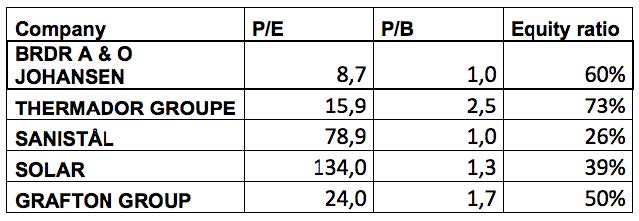

Multiple – valuation metrics, P/E, P/B, P/S and EV/EBITDA.

Looking at the valuation multiples for the company, it seems obvious that it is relatively inexpensive company. All multiples are well below both the peer average and peer median.

– Growth and profit margin

In terms of profitability, Arkil is ranked among the top of its close peers, and well above the industry average and median. If we look at the profitability of the company, this is once again a point of relative strength;

however, there is a large variability within the sector. In terms of growth Arkil seems to be lagging behind its peers, with a geometric growth rate of 1.3% during the last five years against a peer average of 1.9%.

– Capitalization and return metric

Compared to peers, the company has a relatively high proportion of equity financing, this is an equity buffer is a desirable property to have in such a cyclical industry. Nevertheless, this capital structure has resulted in a lower ROE compared to peers.

In conclusion

At a DCF valuation with an up side at 99,7% build up with a conservative estimations and the multiples analysis where Arkil seems relatively inexpensive refer to a expectation that Arkil may be a cheap and solid

investment.

Authors: Allan Gjerløv Jensen, Anders Bager Rasmussen and Christian Montes Schutte