cBrain

Valuation of cBrain on the Danish market

cBrain is a Danish‐based IT company with headquartered in Copenhagen. They have a market value of 138mio DKK. cBrain creates software solutions for primarily 3 main areas: Member Administration and Services, Project Portfolio Management and Digital Management and Processing. cBrains product are today used in 9 Danish Ministry’s including the Prime Minister’s Office.

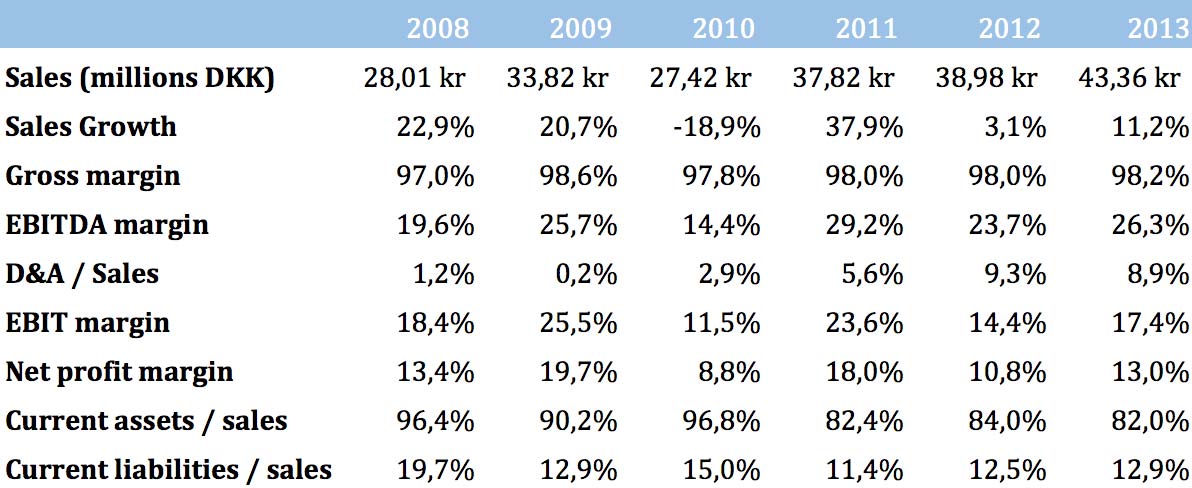

Historically, cBrains sales have on average been increasing over the past six years. cBrain pays dividends equal to a yield of 1% (2013) and seen in this light, the growth rates are very impressive and a rare sight in normal IT growth companies. The primary part of cBrain’s business is located in Denmark, but cBrain is doing promotion in Germany. If they are successful in Germany, it can mean increased sales and higher margins because software in general is easy to scale. The value of the expected German business is uncertain, so we have decided to make two

valuations. One of the Danish business alone and one of the possible German.

The Danish market

In our DCF analysis of the Danish part of cBrain, we assume that cBrain can maintain a growth on average of 11% in revenue over the next six years. This may seem high, but we believe that there is still good growth opportunities in Denmark, because cBrains products currently is being used in the ministries, and we believe it will serve as an endorsement for cBrains. We expect that they can maintain their margins and the depreciation and amortization is maintained proportional constant. We believe that this is a conservative estimate because of the scaling possibilities.

Based on the table above and a budget‐ and a terminal period, we arrive at the following value for the Danish part of cBrain.

The German market

In the last few years, cBrain has worked on entering the German market. In may 2012 cBrain made an important cooperation agreement with the large research organization Fraunhofer with the purpose of introducing the F2 system in the German market. cBrain are still spending significant resources to enter the German market. We have valued the German option using a DCF. The revenue and free cash flow estimated is listed below.

Notice, in the case cBrain successfully enters the German market, we believe the first revenue is collected in 2015 and is growing significantly until 2020. From the year 2020 we assumes a 2% long term growth rate. With a discount rate of 8%, the net present value of the German business is 460 million DKK, equal to 23 DKK per share in cBrain. The likelihood cBrain successfully enters the German market is very difficult to estimated. For the purpose of this valuation, we set the likelihood of success to 33%. In that case, the likelihood adjusted net present value of ‘the German option’ is 153 million DKK or 7,7 DKK per share.

Conclusion

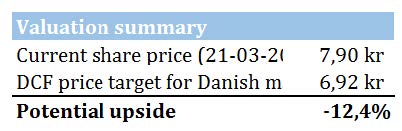

Overall, we believe that cBrain has a fair value of 14.62 DKK. This provides a potential up side of 85%. This estimate is of course subject to some uncertainty, because of the German part of the business, while the Danish part is pretty certain. So our argument is, that we get the Danish business for a little over fair value and then we get the German part as a option, that can give a big potential up‐side.