Brdr. AO

Brdr. A & O Johansen

Brdr. A &O Johansen (AO) distributes and sells plumbing supplies and tools in Denmark (90% of revenue), Sweden and Estonia. In recent years the company has invested heavily in a new efficient warehouse, IT, new stores and upgrades of existing stores. After weathering the financial crisis with minimal losses, the equity ratio, revenue, profits and book value have been rising steadily since. Today AO is in a strong position with high profits, low debt and a strong platform for future growth.

stores and upgrades of existing stores. After weathering the financial crisis with minimal losses, the equity ratio, revenue, profits and book value have been rising steadily since. Today AO is in a strong position with high profits, low debt and a strong platform for future growth.

Strong management team

CEO and major stockowner is Niels A. Johansen, who is 3rd generation of the founder. CFO is Henrik Krabbe who is educated from INSEAD. We believe they make a strong management team with a combination of hands on experience and a strong theoretical background. Sometimes it can cause problems when the CEO is the biggest shareholder, because it

decreases the likelihood the CEO will be fired if he is incompetent, and increases the likelihood the CEO focuses on other goals that creating value for all shareholders. However we are not concerned this is an issue in AO because the chairman of the board is Henning Dyremose, former CEO and chairman of TDC. Dyremose has the experience and clout to be a strong chairman. Overall we are very pleased with the management of AO.

Ownership structure

The founding family controls 52% of the votes through Evoleska Holding AG and thus has full control over the company. Other major shareholders are Sanistål and Lemvigh‐Müller who also both happen to be competitors to AO. AO have not distributed profits to shareholders since the financial crisis and thus have significant financial flexibility today. The flexibility has been build up because AO expects to acquire own stocks from Sanistål who is under financial distress. We expect AO will put their financial flexibility to use in the future, either by acquiring shares from Sanistål or through dividends and share buyback programs.

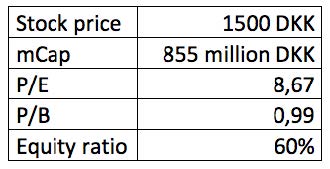

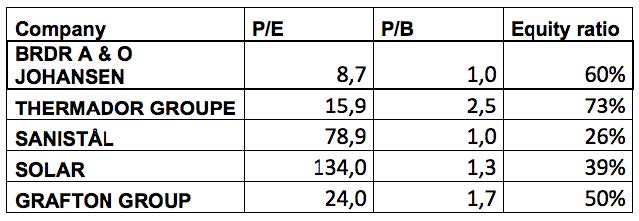

Valuation

The upside in AO based on a discounted cash flow (DCF) analysis is 50%, indicating the company is significantly undervalued. When comparing AO to other companies in their industry, AO also appears to be undervalued. AO is trading at almost half the P/E of the second cheapest company, has a P/B comparable to the distressed Sanistål and has the second highest equity ratio.

Both measured in absolute and relative terms, AO looks significantly undervalued. In addition to the cheap price tag, we find the company to be of high quality in regards to management, financial strength and investments in the future. We have thus decided to invest in AO.