Zealand Pharma

Business info

Zealand Pharma A/S is a Danish based biopharmaceutical company which is engaged in the discovery, development and commercialization of peptide medicines. Their pipeline contains:

- Lyxumia (Lixisenatide)–At the market

- Lyxumia/Lantus (Lixilan)–Phase III

- ZP2929–Phase I

- Danegaptide–Phase II

- Elsiglutide–Phase II

The overall pipeline includes cardio-metabolic diseases that are the underlying medicine for diabetes, and obesity treatment and the company’s most valuable partner right now is Sanofi who is handled with the products Lixisenatide and LixiLan.

Exposition of the pipeline

-Lixisenatide

The product Lixisenatide is a drug for treatment of adults with Type 2 diabetes. In 2013,Lixisenatide was approved in both Europe and Japan and under regulatory review in anumber of other countries globally, paving the way for future sales growth. A general industryconsensus believes that once the product is approved in US (the worlds largest market fordrug of insulin), the sales will accelerate, leading to forecasted sales of € 696 mill. in 2018. Inour forecasted model, only a one-time milestone payment of € 19 mill. is incorporated, sinceLixisenatide is already a marketable product. The specific agreements regarding royaltyrevenues are unavailable for the public, but lies in the low-double-digit region. Based on thelittle given information, a fair estimate is royalty revenue of 15% of total sales. Due to the factthat the product is already marketable in Europe and Japan, and is expected to apply forregistering in the US in summer 2015, the probability of receiving the royalty revenues isfairly high compared to some of Zealand Pharma’s other products.

-LixiLan

This is a combination product of Lixisenatide and Sanofis Lantus. In the following two years,the key driver of expected income is milestone payments. LixiLan is currently in Phase III, andregulatory filings are expected to occur late 2015. Our sales forecast is based on theexpectation that LixiLan is marketable from 2016, which is also the last year that LixiLan willreceive milestone payments. The unpredictable nature of pharmaceuticals has made us relyon analyst consensus reports. Total sales in 2018 are expected to be € 734 mill. After 2018,the sales are forecasted to grow at the rate of inflation. Royalty revenues are expected to be15% of total sales, and the probability of receiving the milestone payments is considered to berelatively high. Due to the late development stage of LixiLan, and the fact that Sanofi is astrong market player, the optimism for the products succes in the market is rather high.

-ZP2929

The product ZP2929 is a drug for diabetics and obesity. The market is fast changing with many players, so naturally it is hard to find the money to develop the drug. Zealand recently lost Boehringer as their partner due to better potential in another drugs.

The main factor of the cash flow is the milestones from partners and we see low likelihood of a new partner for ZP2929, a once-daily glucagon injection, is a lesser attractive investment than the brand new drug in process of Zealand, a glucagon tablet that require no injection. As this new drug just emerged, we can only expect low cash flow with low probability of reaching the market and hence we tried to include this in the cash flow of ZP2929. We set a chance of obtaining a new partner to 15%.

Assuming the maximum sales is the sales of Novo Nordic’s Victoza we projected the royalties of ZP2929 that is, according to the previous Boehringer deal, is “… a high single to low double digit of global sales”. As the product is estimated to reach the market in 2021 and the similar Victoza already in stores, the sales are expected to be 15% of Victoza.

– Danegaptide This drug can bring oxygen to the heart musculature. The realty of the product is dependent on finding a partner who can truly or partial pay for the cost to take the drug to the next phase. The probability is expected to 20% because Danegaptide has succeeded in a lot of tests, which probably will make the attractive for a new partner to make a partnership. But of cause there is a risk.

-Elsiglutide

This is a drug to treat diarrhoea, which can break out under chemotherapy. The drug is not dependent of partnership agreement probability because Zealand Pharma already works together with Helsinn. The drug is only at phase II that makes a probability for succeed the coming phases approximately a bit under 50%, which makes the future milestone earnings less likely. Because the expected royalties for the product first lie in the future (expected six to eight years from 2014) and the probability to get the permission is estimated to be very low, the net present value of future royalties are very low. The induced milestone earnings are the most important earnings for Elsiglutide.

Cash burn

The company has a yearly cash burn of approximately € 24 mill. The majority is spent on research and development (€ 20 million) but administration cost is also significant (€ 4 mill.). With cash position of € 40 mill., Zealand Pharma can run 20 months without income or new capital. However Zealand Pharma is collecting significant revenue from milestones and is in addition starting to earn royalties. As long as Zealand Pharma has moderate success with their drugs going forward, we do not expect them to need to raise new capital.

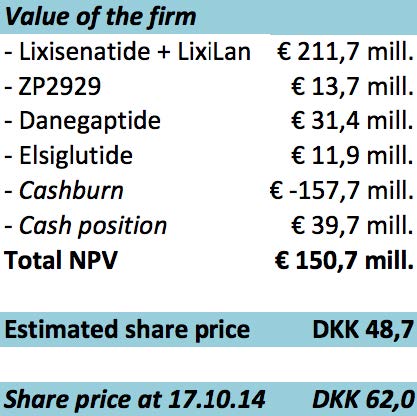

As seen on the figure above, the calculation for the company’s valuation ends at a total net present value of € 150,7 mill. which corresponds to a share price of DKK 48,7.

The conclusion of the valuation is clear, we recommend to not invest in the company, because the expected share price is DKK 48,7 and todays share price is DKK 62,0. It is important to underline the relatively high uncertainty of the future earnings, given the heavy reliance on the outcome of clinical tests.

Authors Allan Gjerløv Jensen, Thomas Tang Axelsen